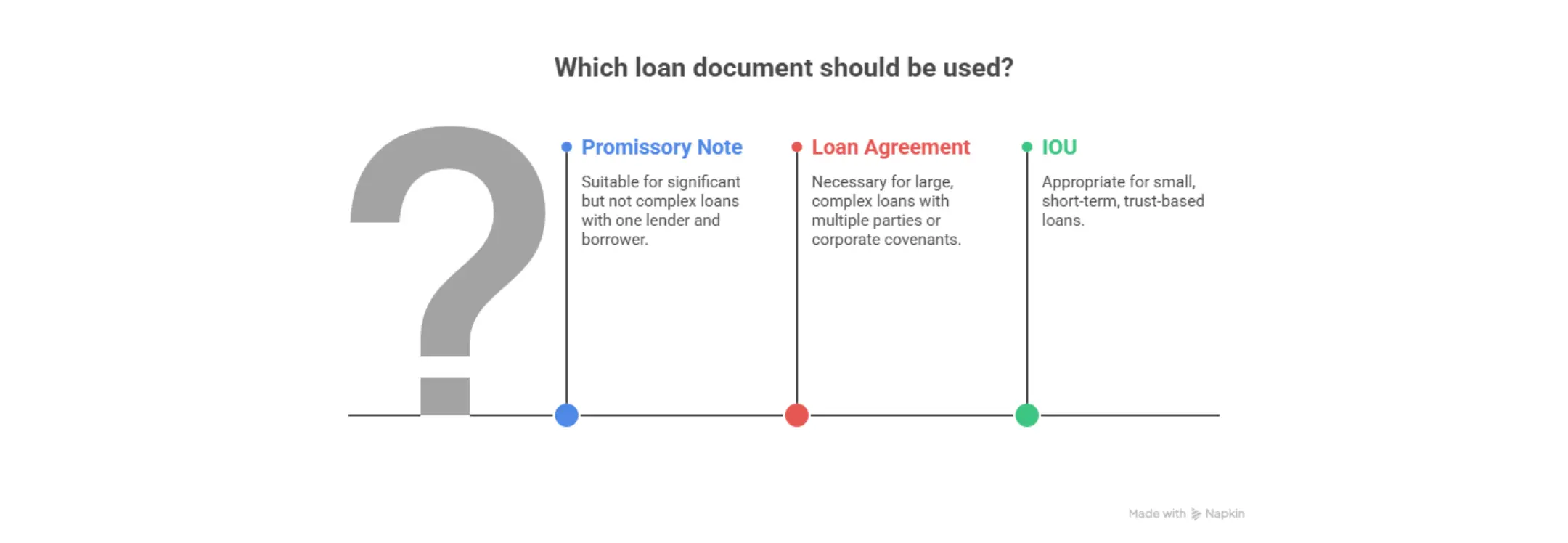

TL;DR - A Promissory Note is a written promise to repay a defined amount with clear terms, and it is generally enforceable in court when drafted correctly.

- A loan agreement is a more complex contract that adds detailed covenants, representations, and remedies around the loan relationship, usually for higher risk or higher value deals.

- An IOU is mainly an acknowledgment that money is owed and often lacks repayment, interest, and default clauses, which makes enforcement and collection much harder.

- Promissory Notes sit between simple IOUs and full loan agreements and work well for many personal, private, or small business loans that still need structure.

- Using an Online Promissory Note template from Ziji Legal Forms with clear repayment, interest, and default terms reduces ambiguity and helps protect both sides if something goes wrong.

Why These Three Documents Get Confused?

For non lawyers, all three documents appear to do the same thing. They show that someone owes money. The differences only become obvious when payments are late, a relationship breaks down, or a lender tries to enforce repayment. Courts look at content, not labels. A document called an IOU that actually contains detailed loan terms might be treated more like a promissory note, while a so called note that only says “I owe you money” may be viewed as too vague to support full enforcement.

Understanding the structural differences before anyone signs helps match the document to the loan’s size, risk, and relationship dynamics. That planning step is often the difference between a clear path to repayment and months of argument over what the parties really agreed.

What is a Promissory Note

A promissory note is a written promise by a borrower to repay a specific principal amount, usually with interest, on defined terms. When properly drafted, it functions as a stand alone legal instrument that a lender can present in court to prove the debt, the repayment schedule, and the default situation.

Promissory notes are common for structured but still relatively simple loans. Examples include personal loans between family or friends, small business funding from private investors, or peer to peer lending where the parties want more than an informal IOU but less complexity than a full commercial loan agreement.

Because a promissory note usually focuses on payment terms rather than broader business covenants, it is easier to prepare and understand while still giving both sides a clear blueprint for repayment and default remedies.

What is a Loan Agreement

A loan agreement is a comprehensive contract that governs the entire lending relationship, not just the promise to repay. In addition to principal, interest, and term, it often includes representations and warranties by the borrower, covenants about how the borrower will behave financially, conditions for advancing funds, and detailed remedy provisions for default.

Banks, institutional lenders, and parties dealing with large or complex loans rely on these agreements because they want more control and more protective detail. The borrower might agree to maintain certain financial ratios, provide periodic financial statements, avoid additional debt without consent, or keep collateral insured.

This additional structure comes with more complexity and preparation time, but it allows the lender to monitor risk and act proactively if the borrower’s financial condition or behavior changes in worrying ways.

What is an IOU

An IOU is usually a simple statement that one person owes another a certain amount of money. It might say who owes, who is owed, and how much, without specifying interest rates, due dates, or what happens if the borrower does not pay.

Because IOUs are so bare, they may be sufficient for small, short term, trust based loans where both sides are confident in repayment and do not expect to involve lawyers or courts. However, that same simplicity becomes a weakness when circumstances change. Without clear terms, it is harder to prove that a payment was late, that interest is owed, or that penalties apply.

As a result, IOUs offer the least legal protection and are more likely to generate disputes about what was intended if repayment time arrives and the borrower does not follow through.

Key Differences in One View

Enforceability and Detail

A well drafted promissory note spells out principal, interest, repayment schedule, and default triggers, which makes it relatively straightforward to enforce if needed. A loan agreement adds layers of detail around conduct, disclosures, and collateral, increasing lender protection and complexity.

An IOU, by contrast, often leaves important questions unanswered. Without clear due dates or default language, a court may have to infer terms or treat the document as only partial evidence of an obligation.

Risk Exposure and Flexibility

For lenders, a loan agreement provides the most control and lowest risk, particularly in large or multi party deals. A promissory note still offers meaningful protection but with fewer moving parts and a narrower focus on repayment. An IOU leaves the lender exposed to interpretive risk and weak remedies if repayment stalls.

Borrowers gain flexibility with simple IOUs but at the cost of unclear expectations. With a promissory note, they trade some informality for clarity, often a worthwhile exchange when the stakes are significant.

When a Promissory Note Is the Right Choice

A promissory note is often the best fit when a loan is significant enough that both parties care about repayment discipline, but not so large or complex that a full loan agreement is needed. Typical examples include private loans between individuals, early stage funding for small businesses, or loans where there is one lender and one borrower and collateral, if any, is simple.

In these cases, the promissory note template can capture essential terms like amount, interest rate, payment frequency, maturity date, late fees, default triggers, and whether the note is secured, all in a digestible format. This structure protects the lender while giving the borrower a clear roadmap of what is expected.

When a Loan Agreement Makes More Sense

For large loan amounts, deals with multiple lenders or investors, or transactions that intersect with corporate covenants, a loan agreement is usually more appropriate. The lender may want assurances about how the business will operate, limits on additional borrowing, or rights to step in if certain financial metrics are not met.

High risk loans, such as those to startups with volatile cash flow or complex collateral structures, also often call for loan agreements. The extra legal detail can help avoid disagreements about what rights the lender has if the borrower’s performance deviates from expectations.

When an IOU May Be Enough

In very small, short term, and trust based situations, a simple IOU may be sufficient. Examples include a modest cash loan among close friends for a near term need or a small advance expected to be repaid with a single paycheck.

Even then, writing down at least the amount, basic timing, and any interest helps avoid misunderstandings. But when the probability of legal enforcement is low and the cost of drafting more formal documents would exceed the loan value, parties sometimes accept the trade off and use an IOU.

Risks of Choosing the Wrong Document

If a loan that should have been captured in a promissory note is instead evidenced only by an IOU, the lender may face serious difficulty enforcing repayment. Missing repayment schedules, interest terms, or default provisions can give borrowers room to argue about what was promised and when payment is truly due.

Conversely, using a complex loan agreement where a simple note would have sufficed can slow down funding, increase professional costs, and discourage borrowers from entering the deal at all. Overcomplicating low risk loans can be just as problematic as under documenting high risk ones. The goal is to match the document to the transaction’s size and stakes.

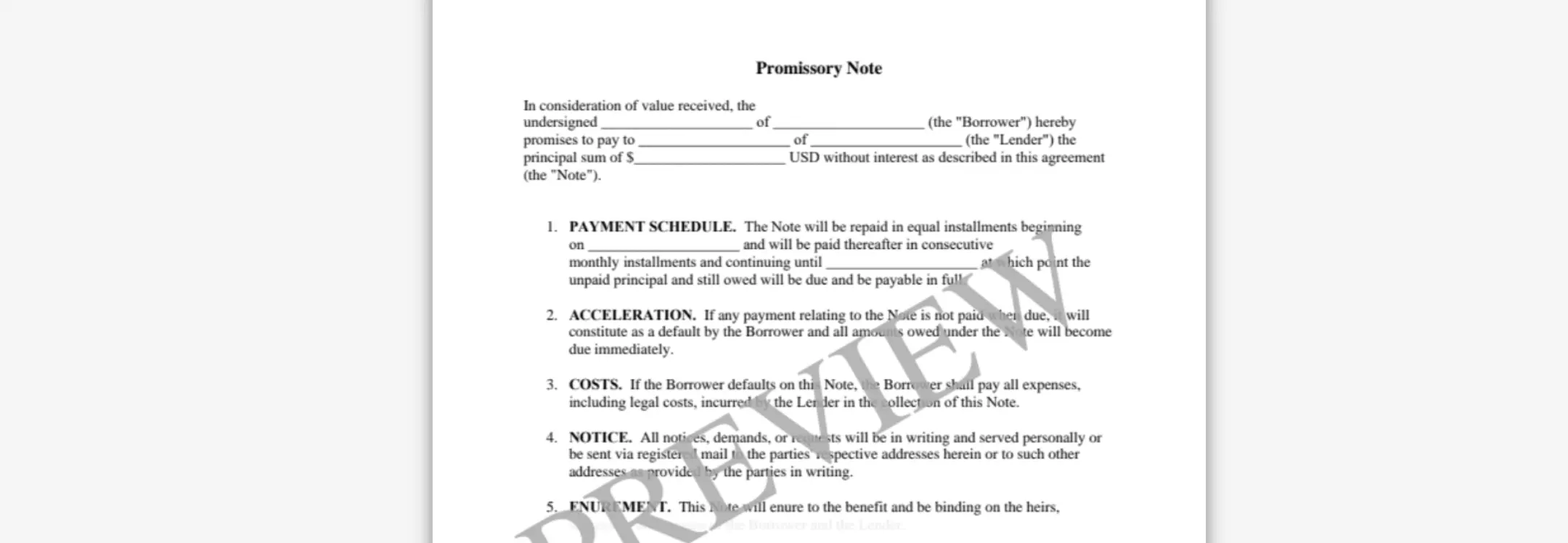

How to Create a Promissory Note with Ziji Legal Forms

1. Choose template

Select the online promissory note template on Ziji Legal Forms

2. Add Party Details

Enter full legal names and contact information for lender and borrower, and include any co signers so that responsibilities are clearly assigned.

3. Add Term Details

Specify principal, interest rate, payment schedule, due dates, late fees, default events, and whether the promissory note will be secured or unsecured.

4. Preview and Print

Review the completed online promissory note for accuracy and clarity, then download a final version as a PDF for signing and safekeeping by both parties.

Ziji Legal Forms' structured promissory note template focuses on clarity and enforceability, helping both sides avoid the common gaps that plague informal IOUs and loosely drafted promises.

Conclusion: Choose the Level of Structure Your Loan Deserves

Promissory notes, loan agreements, and IOUs are not interchangeable labels. Each carries a different balance of simplicity, protection, and enforcement strength. By matching the document type to the loan’s size and risk, and by using a clear online promissory note when appropriate, lenders and borrowers can reduce disputes and protect relationships along with their money.

Promissory Note FAQs

What is a promissory note also known as?

A promissory note is also known as the following: demand note, IOU “I owe you”, loan agreement, or promise to pay agreement.

What is a promissory note?

A promissory note is a legal instrument where the borrower promises to repay the loan owed to the lender under the terms of the note. It’s essentially a promise to repay the lender.

Who is a co-signer for the promissory note?

The co-signer, also called a guarantor, is someone who is guaranteeing the loan and will be responsible for paying for the full amount of the loan if the borrower cannot repay the loan to the lender.

What should the promissory note cover?

The promissory note typically contains the following terms:

- the original loan amount

- interest payment, if any

- repayment schedule

- late fees, if any

- collateral for the loan, if any

You can use our template and create a promissory note with the following steps:

- Select the loan’s location

This is the state where the lender lives and the promissory note will be customized to that jurisdiction.

- List the parties to the loan

Provide the names and addresses of the lender and the borrower. You may also include a co-signer or guarantor if there is one.

- List the terms of the loan

Describe how much is the loan amount. Secondly, is interest being charged? If so, what percentage will the interest be and how will the interest be calculated and accrued. Thirdly, list the repayment schedule. Typically, loans are repaid in instalments and payments can be made weekly, monthly, quarterly, semi-annually or yearly. However, the loan can also be repaid in one lump sum, or at a later date based on the lender’s demand. You will also need to list the first and final payment date to the loan repayment schedule.

- List the prepayment teams

Loans can have prepayment penalty if the borrower repays it early because most lenders are interested in earning the most interest with the loan. You can decide whether to have a prepayment penalty in customizing this promissory note.

- Collateral

A collateral is an asset the lender accepts as security for a loan in case the borrower fails to repay the loan. This is typically reserved for risky borrowers that may not be as credit worthy and who tries to borrow a substantial amount of money. For example, the borrower can use a car, or jewellery as collateral and upon default of the loan, the lender can go to small claims court to seize the collateral or other assets from the borrower in order to satisfy the failure of repayment.

If there is collateral to the loan, describe the collateral in detail to ensure there is no ambiguity what property is being used as collateral. For example, listing the year, make and model of the car, along with the VIN number. If it’s a piece of electronics, list the serial number etc.

Do I need to notarize my promissory note?

You only need the signature of the lender and borrower to have an enforceable promissory note. However having a notary to witness the document adds another layer of authenticity and protection in case the loan gets disputed in court in the future. For loans involving substantial amount of money, it may be prudent to have it notarized.

Can a promissory note be modified after it is signed?

Yes, a promissory note can be changed or amended if both the lender and borrower agree to the new terms. Any modifications should be documented in writing and signed by both parties to avoid confusion or disputes later on.

What happens if the borrower misses a payment?

If the borrower fails to make a scheduled payment, the lender may charge late fees if specified in the note. Repeated missed payments could lead to default, giving the lender the right to demand the full remaining balance immediately or take legal action to recover the debt.

Is interest always required on a promissory note?

No, interest is not mandatory on a promissory note. Some loans may be interest-free, especially between family or friends. However, if interest is charged, the note should clearly state the interest rate and how it will be calculated.

What is the difference between a secured and unsecured promissory note?

A secured promissory note is backed by collateral, meaning the lender can seize specific assets if the borrower defaults. An unsecured promissory note has no collateral backing, so the lender’s remedy is limited to suing the borrower for repayment.

Can a promissory note be transferred to someone else?

Yes, promissory notes can sometimes be assigned or sold to a third party. This means the new holder of the note can collect payments instead of the original lender. The transfer should be documented properly to ensure the borrower knows who to pay.

What jurisdictions can use our promissory note?

You can use our template to create a legal and valid promissory note for the following jurisdictions:

Alabama Alaska Arizona Arkansas California Colorado Connecticut Delaware District of Columbia Florida Georgia Hawaii Idaho Illinois Indiana Iowa Kansas Kentucky Louisiana Maine Maryland Massachusetts Michigan Minnesota Mississippi Missouri Montana Nebraska Nevada New Hampshire New Jersey New Mexico New York North Carolina North Dakota Ohio Oklahoma Oregon Pennsylvania Rhode Island South Carolina South Dakota Tennessee Texas Utah Vermont Virginia Washington West Virginia Wisconsin Wyoming | AL AK AZ AR CA CO CT DE DC FL GA HI ID IL IN IA KS KY LA ME MD MA MI MN MS MO MT NE NV NH NJ NM NY NC ND OH OK OR PA RI SC SD TN TX UT VT VA WA WV WI WY |