TL;DR- Secured promissory notes are backed by collateral like real estate, vehicles, or equipment that lenders can claim if borrowers default on repayment obligations

- Unsecured promissory notes rely solely on the borrower's promise to repay without any collateral backing, making them riskier for lenders

- Secured notes typically offer lower interest rates because collateral reduces lender risk, while unsecured notes require higher interest rates to compensate for increased default risk

- Secured notes work best for large loans or business financing where significant collateral can be pledged, while unsecured notes suit smaller personal loans between trusted parties

- Lenders can repossess collateral from secured notes if borrowers default, but must pursue court action for unsecured notes with uncertain asset recovery prospects

- Ziji Legal Forms provides templates for both secured and unsecured promissory notes ensuring all required provisions are included for either loan type

Introduction: Choosing the Right Promissory Note Type

Selecting the correct promissory note type fundamentally affects how loans function and what protections both lenders and borrowers receive. A secured promissory note backs the loan with valuable assets, while an unsecured promissory note relies entirely on the borrower's creditworthiness and promise to repay.

Understanding these critical differences ensures both parties select the appropriate note type that matches their financial situation, loan amount, relationship, and risk tolerance. The wrong choice can lead to inadequate protection for lenders or unnecessary collateral risks for borrowers.

What Is a Secured Promissory Note

How Collateral Reduces Lender Risk

A secured promissory note is a written agreement where the borrower pledges valuable property as collateral to guarantee repayment. If the borrower defaults, the lender gains legal rights to seize and sell the collateral to recover the loan amount.

Collateral might include real estate, vehicles, equipment, jewelry, stocks, or other valuable assets. The collateral value should equal or exceed the loan amount to provide full protection. If collateral value falls short of the loan amount, the lender's risk increases correspondingly.

Common Collateral Types

Real estate represents the most common collateral for large loans, offering substantial value and clear legal title transfer mechanisms. Vehicles serve as collateral for auto loans, equipment for business financing, and jewelry or personal property for smaller secured loans.

Business assets like inventory, accounts receivable, intellectual property, or equipment provide collateral for commercial secured notes. Choosing appropriate collateral depends on the loan amount, the asset's liquidity, and whether the collateral is easily valued.

Benefits for Borrowers

Secured notes offer significantly lower interest rates because lenders face reduced default risk. Borrowers with substantial collateral can access larger loan amounts on more favorable terms than they could obtain through unsecured borrowing. Longer repayment periods become possible because lenders accept reduced risk, enabling more manageable monthly payments.

Borrowers with limited credit history can sometimes obtain secured loans more easily by pledging collateral as proof of commitment. This provides credit-building opportunities for those with poor or nonexistent credit histories.

What Is an Unsecured Promissory Note

Reliance on Borrower Credibility

An unsecured promissory note creates a loan obligation with no collateral backing. The lender depends entirely on the borrower's promise to repay and their financial ability to meet obligations.

Unsecured notes rely heavily on the borrower's creditworthiness, income stability, employment history, and demonstrated financial responsibility. Lenders assess whether borrowers have sufficient income to service the debt and a track record of honoring financial obligations.

Typical Use Cases

Unsecured promissory notes work well for loans between family members or trusted friends where collateral would undermine the personal relationship. Small business loans between established partners often use unsecured notes because the business relationship itself provides credibility.

Personal loans for consolidating existing debt, covering unexpected expenses, or funding education often utilize unsecured notes. Employee loans from employers typically remain unsecured, relying on employment relationships and paycheck security.

Risk Profile for Lenders

Unsecured lenders face substantially higher default risk because they lack collateral fallback if borrowers cannot or will not repay. If borrowers default, lenders must pursue legal collection action, filing lawsuits to obtain judgments and then attempting to attach assets or garnish wages.

Even successful legal judgments may prove uncollectible if borrowers lack sufficient assets. Filing bankruptcy allows borrowers to potentially discharge unsecured debts entirely, leaving lenders with substantial losses.

Key Differences Between Secured and Unsecured Notes

Collateral Backing

The fundamental distinction between these note types is the presence or absence of collateral. Secured notes explicitly identify, describe, and value collateral that secures the obligation. Unsecured notes contain no collateral provisions whatsoever.

Collateral creates enforceable lender rights to repossess property if defaults occur, while unsecured lending provides only general claims against borrower assets if legal action becomes necessary.

Risk Levels and Protections

Secured lending reduces lender risk dramatically through collateral claims that provide certain recovery mechanisms. Unsecured lending increases lender risk substantially, offering only legal claims against potentially nonexistent or protected borrower assets.

This risk differential directly impacts lending willingness, loan amounts available, and interest rates charged. Lenders willingly accept lower interest rates on secured loans because risk is substantially lower.

Interest Rate Implications

Secured promissory notes typically offer interest rates two to five percentage points lower than equivalent unsecured loans. A borrower obtaining a secured loan at eight percent might pay twelve to fifteen percent for an identical unsecured loan.

Higher unsecured interest rates compensate lenders for increased default risk and the costs of potential collection litigation. Even borrowers with excellent credit pay premium rates on unsecured borrowing compared to secured alternatives.

Default and Enforcement Options

Secured lenders can repossess collateral following defaults, liquidating property to satisfy loan obligations without court involvement in many cases. Unsecured lenders must sue borrowers, obtain judgments, and then pursue collection against available assets through wage garnishment or asset attachment.

Unsecured collection proves slow, expensive, and frequently unsuccessful, especially if borrowers lack substantial assets. Secured collection is faster, more certain, and less costly.

Loan Amounts and Terms

Secured lending enables significantly larger loan amounts because collateral covers lender exposure. Unsecured loans typically remain smaller because lenders limit exposure to amounts they can afford to lose if collection fails.

Repayment terms on secured loans extend longer, sometimes twenty to thirty years for real estate secured mortgages, compared to unsecured loans typically ranging from three to seven years.

When to Use a Secured Promissory Note

Large Loan Amounts

Use secured notes when loan amounts are substantial. Lenders require collateral protection for amounts exceeding borrower annual income or exceeding amounts they could collect if defaults occur.

Business expansion loans, equipment purchases, real estate acquisitions, and other major capital investments typically utilize secured notes. The collateral value should match or exceed the loan amount to provide adequate protection.

Business Transactions and Asset Purchases

Loans directly tied to asset purchases naturally utilize secured notes with the purchased asset serving as collateral. Equipment financing uses the equipment as collateral. Real estate loans use the property as collateral. Inventory financing uses the inventory as collateral.

These arrangements align collateral value with loan purpose, ensuring collateral exists to repay loans. The purchased asset itself becomes the security interest.

Limited Borrower Credit History

Borrowers with poor credit scores or limited credit history can access secured financing when collateral substitutes for creditworthiness. First-time borrowers and individuals rebuilding credit after financial problems can obtain secured loans more easily than unsecured alternatives.

This provides credit-building opportunities while protecting lenders through collateral security. As credit improves, borrowers can eventually refinance into unsecured loans at better rates.

Lender Protection Preference

Any lender preferring maximum protection should require collateral. Real estate professionals financing properties, automotive lenders, equipment manufacturers extending credit all prefer secured arrangements protecting their financial interests.

Risk-averse lenders consistently choose secured over unsecured lending regardless of borrower creditworthiness.

When to Use an Unsecured Promissory Note

Small Personal Loans

Unsecured notes suit smaller loan amounts between family members or close friends where collateral would be inappropriate. Personal loans for unexpected expenses, holiday purchases, or minor emergencies typically utilize unsecured notes.

Loan amounts typically remain modest, under ten thousand dollars, making complete default losses manageable for lenders. Higher interest rates compensate lenders for uncollateralized risk.

Strong Personal or Professional Relationships

Use unsecured notes when both parties have established relationships demonstrating trustworthiness and reliability. Family loans, loans between long-term business partners, and employee loans often utilize unsecured notes based on relationship history.

These relationships often provide informal enforcement mechanisms through social pressure and relationship preservation incentives beyond formal legal remedies.

Excellent Borrower Credit and Income

Borrowers with exceptional credit scores and stable, substantial income can often obtain unsecured loans at reasonable rates. Credit history and income documentation provide sufficient assurance of repayment without collateral requirements.

Excellent creditworthiness sometimes commands unsecured loan terms competitive with lower-quality secured loans when lenders have high confidence in repayment ability.

Situations Where Collateral Is Unavailable

Borrowers without substantial assets sometimes use unsecured notes because they lack collateral to pledge. Individuals early in careers or those who have not yet accumulated property may have no viable collateral options.

In these situations, unsecured notes provide the only available borrowing mechanism regardless of preference.

Advantages and Disadvantages Comparison

Secured Note Advantages

Lower interest rates, access to larger loan amounts, longer repayment terms, and improved lender approval likelihood represent key advantages. Borrowers gain financing access they might otherwise be unable to obtain while reducing total interest costs through lower rates.

Lenders gain certainty of repayment and clear enforcement mechanisms if defaults occur. Risk reduction allows more favorable loan terms benefiting both parties.

Secured Note Disadvantages

Collateral requirements prevent borrowing without significant assets. Defaulting borrowers lose pledged property, creating hardship. Collateral must be identified, valued, and secured through legal documents creating administrative complexity and cost.

Borrowers may resist pledging valuable assets even when beneficial loan terms justify the risk.

Unsecured Note Advantages

No collateral requirements make borrowing accessible to those without significant assets. Simplicity and faster execution reduce administrative burden and costs. Borrowers retain ownership and use of all property.

Informal enforcement between trusted parties proves less expensive than formal collection litigation.

Unsecured Note Disadvantages

Higher interest rates increase total borrowing costs compared to secured alternatives. Smaller available loan amounts limit capital access. Shorter repayment terms create higher monthly payments. Lenders face significant default risk if borrowers cannot or will not repay.

Collection challenges make default recovery difficult and expensive for lenders.

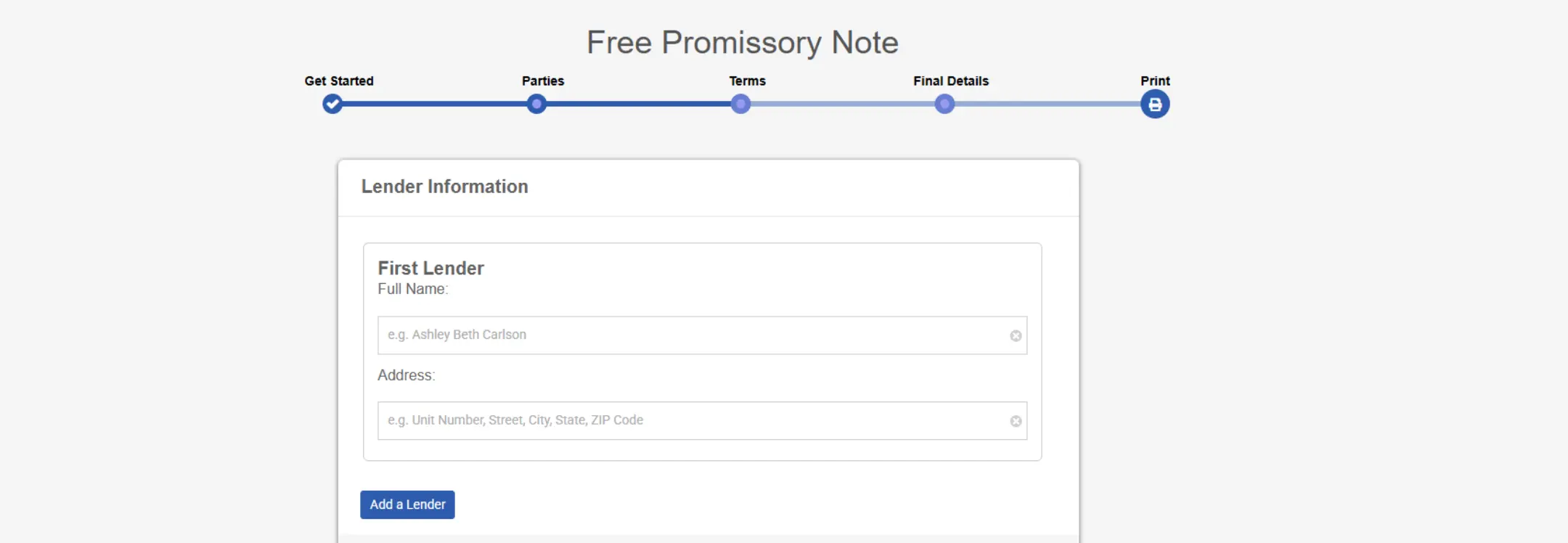

How to Create Promissory Notes Using Ziji Legal Forms

1. Choose template

Access Ziji Legal Forms' Financial section and select either the Promissory Note Template depending on whether collateral will secure your loan.

2. Add Parties' Details

Enter the borrower's full legal name, address, and contact information along with the lender's complete information to clearly identify all parties to the loan agreement.

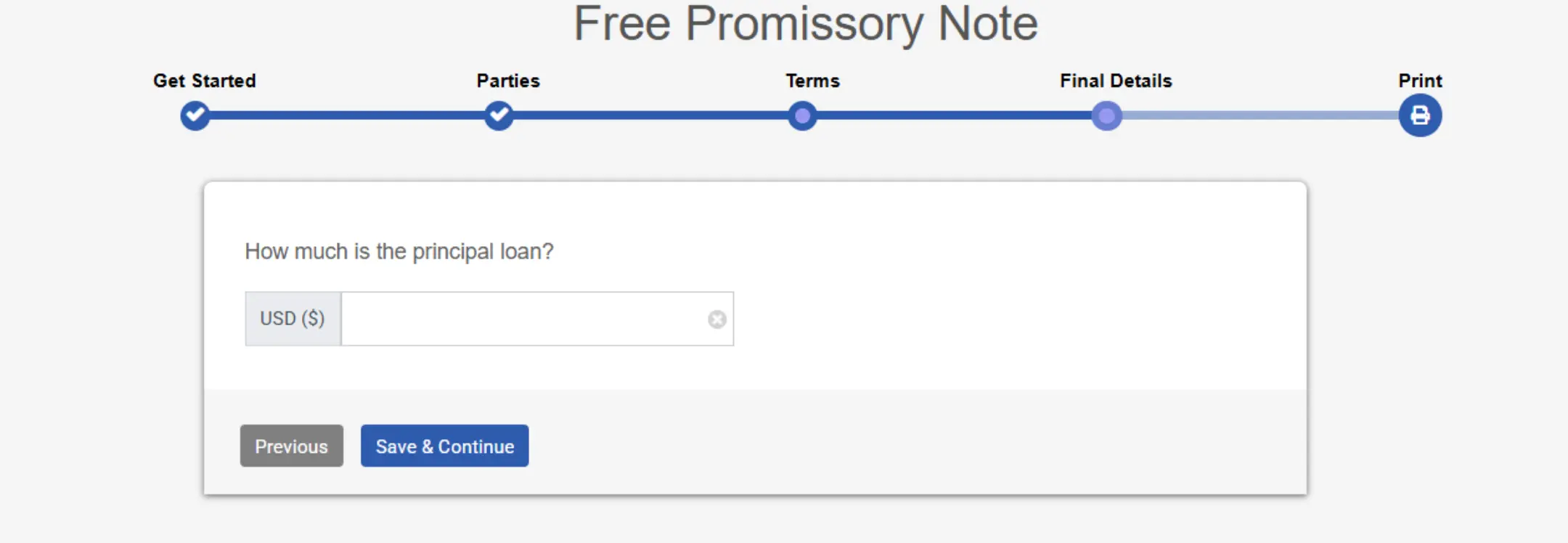

3. Add The Terms

Specify the loan amount, interest rate with clarification about calculation methods, payment schedule with specific due dates and amounts, and late fees or default interest provisions applicable to the note type.

4. Add Final Details

For secured notes, include detailed collateral descriptions with identification information and current valuations. For both types, specify default conditions, enforcement provisions, and governing law.

5. Preview and print.

Review the completed promissory note thoroughly to verify accuracy and completeness, then download in PDF or Word format for signature by both parties with printed names and dates.

Template-Specific Guidance

Ziji's secured note templates include collateral description sections guiding users toward specific identification. Unsecured templates emphasize creditworthiness factors and relationship context. Both templates include all essential loan terms preventing common omissions.

Current templates reflect state-specific requirements and legal standards ensuring enforceability. Built-in provisions address default conditions, interest calculations, and enforcement rights appropriate for each note type.

Conclusion: Choose Your Note Type Based on Your Circumstances

Secured and unsecured promissory notes serve different purposes and protect different interests. Secured notes provide lender protection through collateral while enabling larger loans at lower rates, while unsecured notes suit smaller personal loans based on relationship and creditworthiness. Using Ziji Legal Forms' specialized templates for each note type ensures proper documentation and legal compliance regardless of which note type your situation requires.

Promissory Note FAQs

What is a promissory note also known as?

A promissory note is also known as the following: demand note, IOU “I owe you”, loan agreement, or promise to pay agreement.

What is a promissory note?

A promissory note is a legal instrument where the borrower promises to repay the loan owed to the lender under the terms of the note. It’s essentially a promise to repay the lender.

Who is a co-signer for the promissory note?

The co-signer, also called a guarantor, is someone who is guaranteeing the loan and will be responsible for paying for the full amount of the loan if the borrower cannot repay the loan to the lender.

What should the promissory note cover?

The promissory note typically contains the following terms:

- the original loan amount

- interest payment, if any

- repayment schedule

- late fees, if any

- collateral for the loan, if any

You can use our template and create a promissory note with the following steps:

- Select the loan’s location

This is the state where the lender lives and the promissory note will be customized to that jurisdiction.

- List the parties to the loan

Provide the names and addresses of the lender and the borrower. You may also include a co-signer or guarantor if there is one.

- List the terms of the loan

Describe how much is the loan amount. Secondly, is interest being charged? If so, what percentage will the interest be and how will the interest be calculated and accrued. Thirdly, list the repayment schedule. Typically, loans are repaid in instalments and payments can be made weekly, monthly, quarterly, semi-annually or yearly. However, the loan can also be repaid in one lump sum, or at a later date based on the lender’s demand. You will also need to list the first and final payment date to the loan repayment schedule.

- List the prepayment teams

Loans can have prepayment penalty if the borrower repays it early because most lenders are interested in earning the most interest with the loan. You can decide whether to have a prepayment penalty in customizing this promissory note.

- Collateral

A collateral is an asset the lender accepts as security for a loan in case the borrower fails to repay the loan. This is typically reserved for risky borrowers that may not be as credit worthy and who tries to borrow a substantial amount of money. For example, the borrower can use a car, or jewellery as collateral and upon default of the loan, the lender can go to small claims court to seize the collateral or other assets from the borrower in order to satisfy the failure of repayment.

If there is collateral to the loan, describe the collateral in detail to ensure there is no ambiguity what property is being used as collateral. For example, listing the year, make and model of the car, along with the VIN number. If it’s a piece of electronics, list the serial number etc.

Do I need to notarize my promissory note?

You only need the signature of the lender and borrower to have an enforceable promissory note. However having a notary to witness the document adds another layer of authenticity and protection in case the loan gets disputed in court in the future. For loans involving substantial amount of money, it may be prudent to have it notarized.

Can a promissory note be modified after it is signed?

Yes, a promissory note can be changed or amended if both the lender and borrower agree to the new terms. Any modifications should be documented in writing and signed by both parties to avoid confusion or disputes later on.

What happens if the borrower misses a payment?

If the borrower fails to make a scheduled payment, the lender may charge late fees if specified in the note. Repeated missed payments could lead to default, giving the lender the right to demand the full remaining balance immediately or take legal action to recover the debt.

Is interest always required on a promissory note?

No, interest is not mandatory on a promissory note. Some loans may be interest-free, especially between family or friends. However, if interest is charged, the note should clearly state the interest rate and how it will be calculated.

What is the difference between a secured and unsecured promissory note?

A secured promissory note is backed by collateral, meaning the lender can seize specific assets if the borrower defaults. An unsecured promissory note has no collateral backing, so the lender’s remedy is limited to suing the borrower for repayment.

Can a promissory note be transferred to someone else?

Yes, promissory notes can sometimes be assigned or sold to a third party. This means the new holder of the note can collect payments instead of the original lender. The transfer should be documented properly to ensure the borrower knows who to pay.

What jurisdictions can use our promissory note?

You can use our template to create a legal and valid promissory note for the following jurisdictions:

Alabama Alaska Arizona Arkansas California Colorado Connecticut Delaware District of Columbia Florida Georgia Hawaii Idaho Illinois Indiana Iowa Kansas Kentucky Louisiana Maine Maryland Massachusetts Michigan Minnesota Mississippi Missouri Montana Nebraska Nevada New Hampshire New Jersey New Mexico New York North Carolina North Dakota Ohio Oklahoma Oregon Pennsylvania Rhode Island South Carolina South Dakota Tennessee Texas Utah Vermont Virginia Washington West Virginia Wisconsin Wyoming | AL AK AZ AR CA CO CT DE DC FL GA HI ID IL IN IA KS KY LA ME MD MA MI MN MS MO MT NE NV NH NJ NM NY NC ND OH OK OR PA RI SC SD TN TX UT VT VA WA WV WI WY |