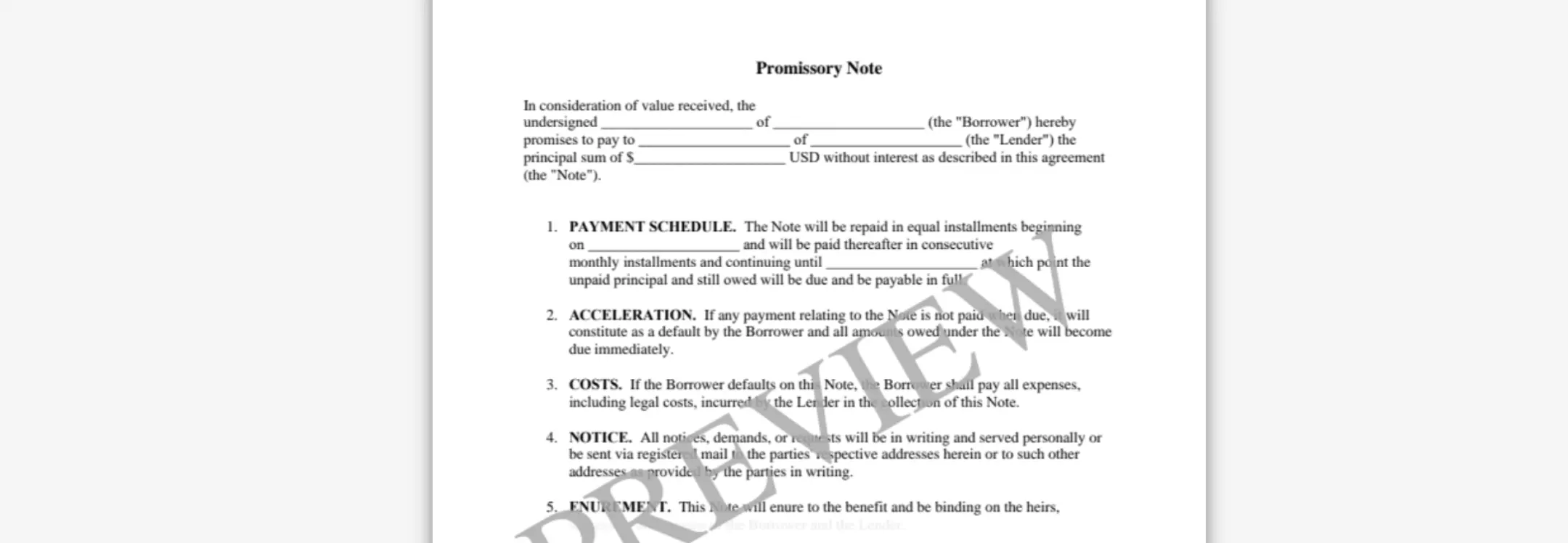

- A Promissory Note is a written promise to repay a specific sum with agreed terms, and non payment can trigger default, acceleration, and legal action.

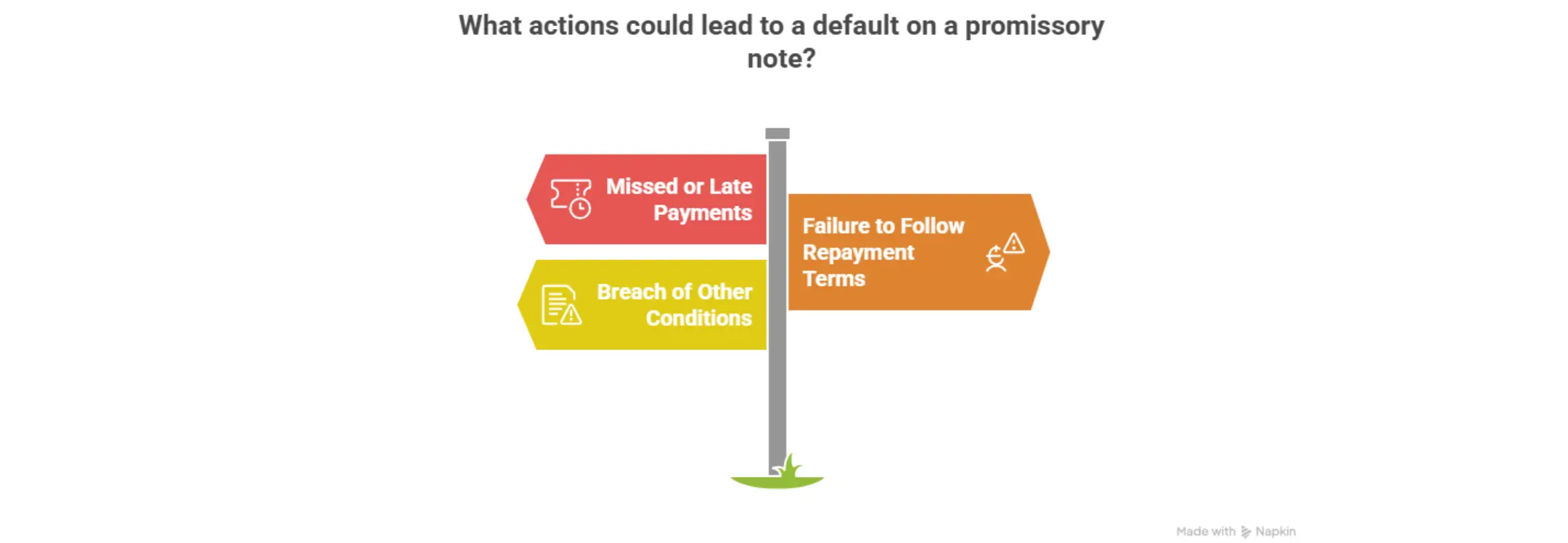

- Default can arise from missed or late payments, breaking repayment terms, or violating other conditions in the Promissory Note template, especially after any grace period expires.

- After default, lenders may send notices, demand full payment, negotiate new terms, or sue, with secured notes also allowing repossession or foreclosure on collateral.

- Secured Promissory Notes give lenders direct rights against specific assets, while unsecured notes require court judgments and collection steps to enforce.

- Borrowers who cannot pay should communicate early, seek modified schedules, and try to avoid judgments that can lead to garnishment and credit damage.

- A clear, well drafted Online Promissory Note with defined default and remedy clauses reduces disputes and makes enforcement more predictable for both sides.

- Creating a clear Online Promissory Note with Ziji Legal Forms helps both parties define payment terms, default triggers, and remedies in a way that is easier to enforce and harder to dispute.

Why Non Payment Consequences Matter Before You Sign

What Counts as a Default on a Promissory Note

Missed or Late Payments

Failure to Follow Repayment Terms

Breach of Other Conditions in the Note

Grace Periods and Acceleration Clauses

How Grace Periods Work

What Acceleration Means

What Happens After a Default Occurs

Notice of Default and Chance to Cure

Loan Acceleration and Demand for Full Payment

Enforcement Options Available to Lenders

Informal Negotiations and Demand Letters

Lawsuits and Judgment Enforcement

Secured Versus Unsecured Promissory Notes

Recovery of Collateral in Secured Notes

Court Based Recovery for Unsecured Notes

Can a Promissory Note Be Enforced in Court

Conditions for Enforceability

Importance of Clear Terms and Valid Signatures

What Borrowers Should Do If They Cannot Pay

Communicate Early with the Lender

Seek Modified Terms

Avoid Escalation and Legal Action

How a Well Drafted Promissory Note Reduces Disputes

How to Create an Enforceable Promissory Note Using Ziji Legal Forms

1. Choose template

2. Add Party Details

3. Add Term Details

4. Preview and print

Conclusion: Treat Non Payment as a Planning Issue, Not Just a Crisis

Promissory Note FAQs

What is a promissory note also known as?

A promissory note is also known as the following: demand note, IOU “I owe you”, loan agreement, or promise to pay agreement.

What is a promissory note?

A promissory note is a legal instrument where the borrower promises to repay the loan owed to the lender under the terms of the note. It’s essentially a promise to repay the lender.

Who is a co-signer for the promissory note?

The co-signer, also called a guarantor, is someone who is guaranteeing the loan and will be responsible for paying for the full amount of the loan if the borrower cannot repay the loan to the lender.

What should the promissory note cover?

The promissory note typically contains the following terms:

- the original loan amount

- interest payment, if any

- repayment schedule

- late fees, if any

- collateral for the loan, if any

You can use our template and create a promissory note with the following steps:

- Select the loan’s location

This is the state where the lender lives and the promissory note will be customized to that jurisdiction.

- List the parties to the loan

Provide the names and addresses of the lender and the borrower. You may also include a co-signer or guarantor if there is one.

- List the terms of the loan

Describe how much is the loan amount. Secondly, is interest being charged? If so, what percentage will the interest be and how will the interest be calculated and accrued. Thirdly, list the repayment schedule. Typically, loans are repaid in instalments and payments can be made weekly, monthly, quarterly, semi-annually or yearly. However, the loan can also be repaid in one lump sum, or at a later date based on the lender’s demand. You will also need to list the first and final payment date to the loan repayment schedule.

- List the prepayment teams

Loans can have prepayment penalty if the borrower repays it early because most lenders are interested in earning the most interest with the loan. You can decide whether to have a prepayment penalty in customizing this promissory note.

- Collateral

A collateral is an asset the lender accepts as security for a loan in case the borrower fails to repay the loan. This is typically reserved for risky borrowers that may not be as credit worthy and who tries to borrow a substantial amount of money. For example, the borrower can use a car, or jewellery as collateral and upon default of the loan, the lender can go to small claims court to seize the collateral or other assets from the borrower in order to satisfy the failure of repayment.

If there is collateral to the loan, describe the collateral in detail to ensure there is no ambiguity what property is being used as collateral. For example, listing the year, make and model of the car, along with the VIN number. If it’s a piece of electronics, list the serial number etc.

Do I need to notarize my promissory note?

You only need the signature of the lender and borrower to have an enforceable promissory note. However having a notary to witness the document adds another layer of authenticity and protection in case the loan gets disputed in court in the future. For loans involving substantial amount of money, it may be prudent to have it notarized.

Can a promissory note be modified after it is signed?

Yes, a promissory note can be changed or amended if both the lender and borrower agree to the new terms. Any modifications should be documented in writing and signed by both parties to avoid confusion or disputes later on.

What happens if the borrower misses a payment?

If the borrower fails to make a scheduled payment, the lender may charge late fees if specified in the note. Repeated missed payments could lead to default, giving the lender the right to demand the full remaining balance immediately or take legal action to recover the debt.

Is interest always required on a promissory note?

No, interest is not mandatory on a promissory note. Some loans may be interest-free, especially between family or friends. However, if interest is charged, the note should clearly state the interest rate and how it will be calculated.

What is the difference between a secured and unsecured promissory note?

A secured promissory note is backed by collateral, meaning the lender can seize specific assets if the borrower defaults. An unsecured promissory note has no collateral backing, so the lender’s remedy is limited to suing the borrower for repayment.

Can a promissory note be transferred to someone else?

Yes, promissory notes can sometimes be assigned or sold to a third party. This means the new holder of the note can collect payments instead of the original lender. The transfer should be documented properly to ensure the borrower knows who to pay.

What jurisdictions can use our promissory note?

You can use our template to create a legal and valid promissory note for the following jurisdictions:

Alabama Alaska Arizona Arkansas California Colorado Connecticut Delaware District of Columbia Florida Georgia Hawaii Idaho Illinois Indiana Iowa Kansas Kentucky Louisiana Maine Maryland Massachusetts Michigan Minnesota Mississippi Missouri Montana Nebraska Nevada New Hampshire New Jersey New Mexico New York North Carolina North Dakota Ohio Oklahoma Oregon Pennsylvania Rhode Island South Carolina South Dakota Tennessee Texas Utah Vermont Virginia Washington West Virginia Wisconsin Wyoming | AL AK AZ AR CA CO CT DE DC FL GA HI ID IL IN IA KS KY LA ME MD MA MI MN MS MO MT NE NV NH NJ NM NY NC ND OH OK OR PA RI SC SD TN TX UT VT VA WA WV WI WY |

Create your

Promissory Note

in minutes

Get Started For Free Related Financial Blogs

If our legal documents helped you today, we’d truly appreciate your feedback.

Your review helps others make informed decisions and helps us improve our platform for everyone.